Subtotal $0.00

Of numerous mortgage loans in australia take attention-only (IO) terminology. Houses remove IO loans for many causes, particularly taxation incentives and payment flexibility. They ensure it is individuals to stay far more indebted for longer and you can involve a considerable step-upwards in needed money (to add prominent) if loan converts so you can getting an excellent P&I loan.

IO finance got adult easily for a number of decades from inside the a world of low financial cost and you will increased aggressive challenges to have the newest funds among loan providers (Chart C1). The newest share from a fantastic construction borrowing on IO words risen to nearly 40 percent by the 2015. The new express into IO words has always been higher to possess traders than simply holder-occupiers (similar to the relevant taxation pros for people). But IO loans to own proprietor-occupiers had also mature highly.

Because of the as long as the IO finance return to help you P&I since the arranged which is impractical it gives a top bound estimate of one’s aftereffect of the fresh changeover in the future

During the 2014 and you may 2015, the newest Australian Prudential Control Expert (APRA) while the Australian Ties and you will Investment Commission (ASIC) grabbed certain tips to bolster sound housing credit strategies, in addition to certain you to inspired IO loans. ASIC including strengthened its position that owner-occupier fund should not has its IO symptoms lengthened past four decades. Then, during the , APRA established a benchmark that authorised put-getting organizations (ADIs) is always to restrict their new IO financing to help you 30 % off full the new residential home loan financing and you will, within this one, they need to tightly do this new IO loans offered during the higher loan-to-valuation percentages (LVRs). Following the introduction of such steps, extremely banks chose to raise rates into IO loans to help you getting about 40 basis issues over rates on the equivalent P&We fund. It’s got contributed to a decrease in this new interest in this new IO money and you can considering present borrowers that have a reward to switch to help you P&I money. Of many home switched voluntarily from inside the 2017 responding to help you prices differentials. Because of this, the newest inventory from IO money overall casing borrowing possess refuted away from next to forty per cent payday loans easy acceptance so you can nearly 31 % as well as the display of brand new IO loans in total approvals possess fallen well below the 31 % restriction.

The fresh new Set aside Bank’s Securitisation Database means that brand new IO several months was because of expire from the 2020 for around several-thirds of the the stock away from securitised IO finance (while the at end December) (Chart C2). This will be in line with IO symptoms generally are as much as five years. The fresh character out-of IO period expiries implies that about $120 billion out of IO loans when you look at the aggregate was arranged to help you move off to P&We financing a-year across the second 36 months, or around seven per cent of one’s inventory regarding houses borrowing from the bank each year. It frequency isnt unmatched. What is more today, yet not, is the fact financing requirements had been fasten next recently. This tightening when you look at the lending standards, combined with ASIC reinforcing their updates one to manager-occupier financing must not have the IO episodes stretched beyond five decades, may affect the skill of specific consumers to give the newest IO period or perhaps to re-finance so you can a P&We financing with an extended amortising period to treat needed payments on the financing.

But not, other things equal, IO financing can hold greater risks in contrast to dominating-and-attract (P&I) finance

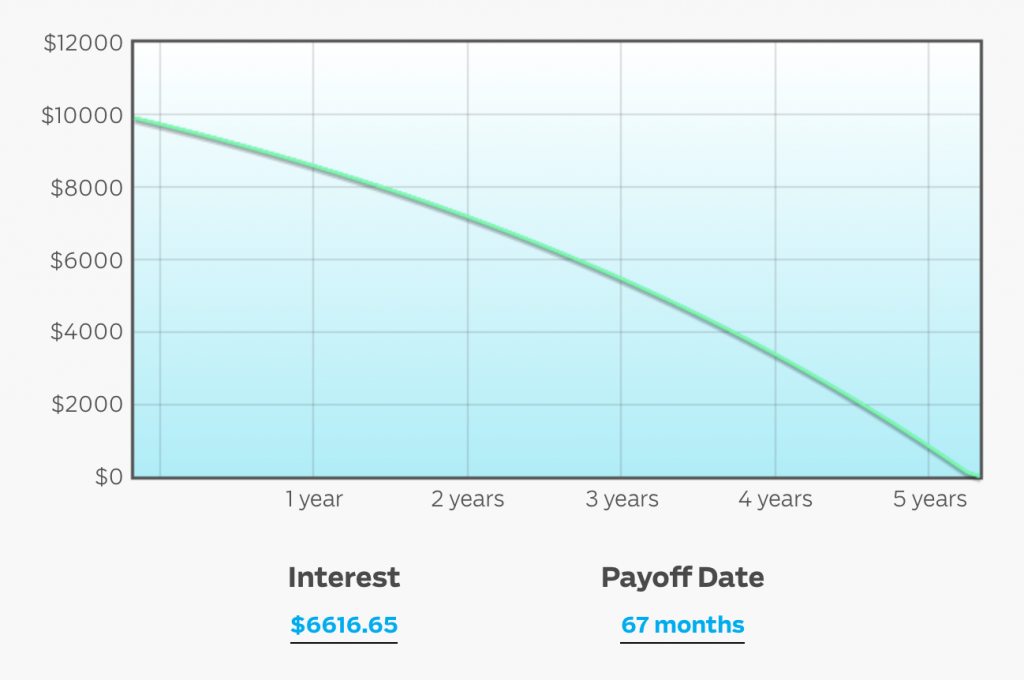

Another simple situation explores the potential effect of the fresh then IO mortgage expiries into households’ cash circulates and you can consumption.

Believe a routine debtor that have a great 5-year IO months to your a thirty-12 months loan and you can an enthusiastic IO interest of 5 %. Like good borrower’s home loan repayments carry out increase because of the as much as 3140 percent whenever the IO period ends plus they start to make P&We money in the a diminished rate of interest of about 4? per cent (Graph C3).